Single member vs multi member LLC taxes differ in ways that become especially important in 2026, as reporting thresholds, filing deadlines, and self-employment tax exposure continue to rise. While both structures are pass-through entities by default, the mechanics of reporting, coordination, and cash planning diverge significantly once a second member is involved.

This guide compares how single-member and multi-member LLCs are taxed in 2026, how income is reported, how self-employment tax applies, and why money-handling discipline matters more as ownership expands.

Income Reporting Differences (2026 Context)

Single-Member LLC

A single-member LLC is treated as a disregarded entity by default. Business income and expenses are reported directly on the owner’s personal tax return.

2026 filing context:

- Standard individual filing deadline: Wednesday, April 15, 2026

- No partnership return

- No Schedule K-1 issued

Income is taxed whether or not cash is withdrawn, but reporting remains centralized under one individual.

Multi-Member LLC

A multi-member LLC is treated as a partnership for federal tax purposes.

2026 filing context:

- Partnership return deadline: Monday, March 16, 2026

- LLC files an informational return

- Each member receives a Schedule K-1

- Members report allocated income on personal returns

This earlier deadline often catches new multi-member LLCs off guard—especially when records or allocations are not finalized early.

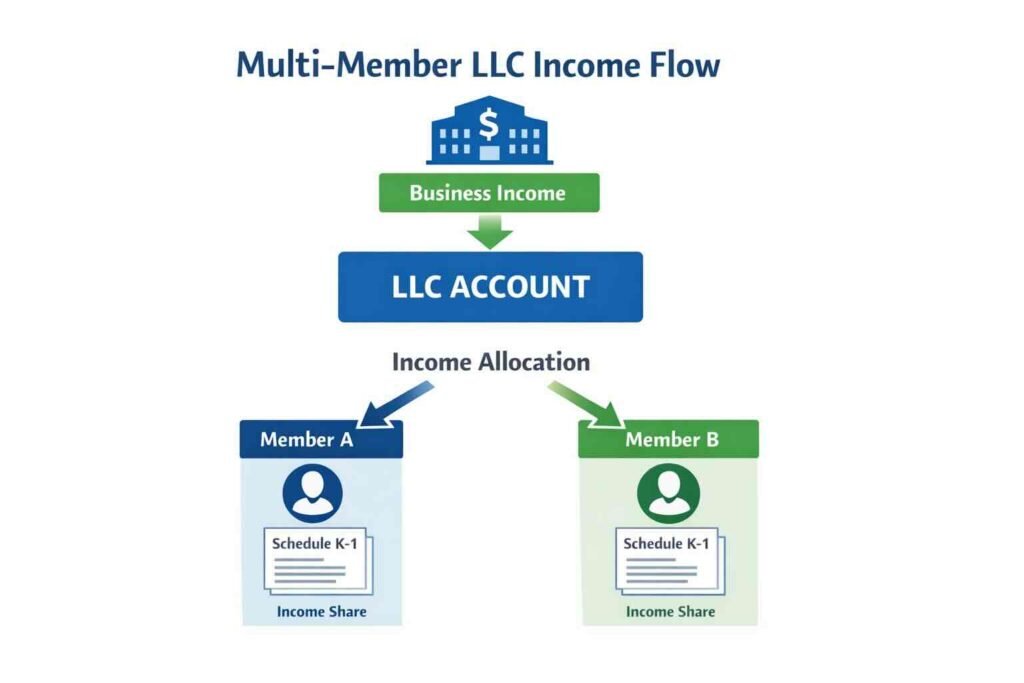

Visualizing the Income Flow (Multi-Member LLC)

A key difference in multi-member LLC taxes is that income and cash do not move together.

ven if money stays in the LLC, income still flows to each member on paper via Schedule K-1. Taxes follow allocation—not withdrawals.

⚠️ Action Step: Handling Checks Correctly

If a client or customer issues a check made out to the LLC:

- Deposit it directly into the LLC’s bank account

- Do not cash it personally

- Do not deposit it into a personal account and “move it later”

This single step preserves clean income reporting and avoids unnecessary commingling or reconstruction later.

The Self-Employment Tax Reality (2026 Update)

Self-employment tax remains one of the most misunderstood aspects of LLC taxation.

2026 Context Note

For 2026, the Social Security wage base has increased to $184,500. Income above this threshold may be treated differently for certain tax components, but self-employment exposure still depends on earned income, not withdrawals alone.

How It Applies

- Single-Member LLC: The owner generally pays self-employment tax on net business income.

- Multi-Member LLC: Active members generally pay self-employment tax on their allocated share of income, regardless of how much cash they actually receive.

This is why owners can face tax obligations even during periods of low distributions.

Allocation and the Operating Agreement (Critical for 2026)

In a single-member LLC, allocation is implicit.

In a multi-member LLC, allocation must be explicit.

Pro tip:

Never assume a 50/50 split. Your Operating Agreement must clearly define how profits, losses, and distributions are handled. If allocation rules are unclear or ignored, Schedule K-1 reporting becomes fragile and disputes become more likely.

Owner Pay Differences

Single-Member LLC

- Owner pay is simpler but still requires discipline

- Transfers should be intentional and labeled

- Reimbursements and owner pay can blur if habits are loose

Multi-Member LLC

- Owner pay requires coordination

- Distributions must align with allocation rules

- Reimbursements, distributions, and capital movements must remain separate

As ownership expands, behavior matters more than structure.

For practical guidance, see:

EIN Requirements Compared

- Single-Member LLC: EIN may be optional in limited cases

- Multi-Member LLC: EIN is mandatory

Multi-member LLCs cannot file partnership returns, issue Schedule K-1s, or operate banking correctly without an EIN.

Why These Differences Matter More in 2026

As income thresholds rise and enforcement becomes more automated, the cost of ambiguity increases. Multi-member LLCs, in particular, face higher friction when money flow, owner pay, or allocation discipline is weak.

The structure you choose determines:

- Filing deadlines

- Reporting complexity

- Cash planning pressure

- Coordination risk

Taxes reflect behavior throughout the year—not just year-end decisions.

Where to Go Next

TTo continue building a solid financial and compliance foundation, explore the LLC Made Easy Education Center, which brings together step-by-step guides on LLC banking, money management, owner pay, and tax structure.

- Multi-Member LLC Taxes Explained (2026 Guide)

- Owner Pay Basics for LLCs

- LLC Money Management Guide

- LLC Banking & Finance Basics

Together, these guides help LLC owners manage taxes intentionally instead of reactively.

Frequently Asked Questions (FAQ)

Disclaimer

This content is provided for general educational purposes only and does not constitute legal, tax, accounting, or financial advice. Tax laws and individual circumstances vary. Consult a qualified CPA or attorney for advice specific to your situation.