Multi member LLC taxes are misunderstood because income, cash, and tax reporting move on different paths. Many owners assume taxes follow withdrawals, or that adding a second member simply means “splitting profits.” In reality, multi-member LLCs introduce income allocation, partnership reporting, and shared tax responsibility—whether or not cash actually changes hands.

This guide explains how multi-member LLC taxes work in practice in 2026: how income is allocated, how self-employment tax applies, how owners are paid, and how this structure differs from a single-member LLC. The goal is clarity, not tax advice—so you understand how the system works before mistakes compound.

How Multi-Member LLCs Are Taxed (Big Picture)

By default, a multi-member LLC is taxed as a partnership.

That means:

- The LLC files an informational tax return

- The LLC itself does not pay federal income tax

- Profits and losses are allocated to members

- Each member reports their share on their personal return

What surprises most owners is that taxes are based on allocation, not withdrawals.

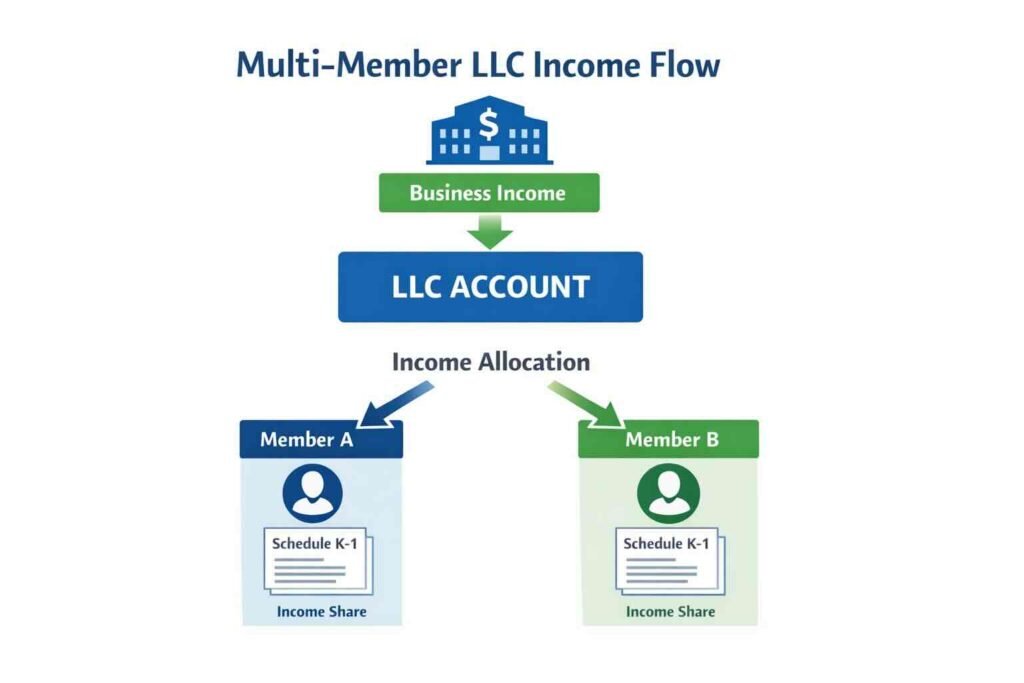

Visualizing the Flow (Mental Model)

Think of multi-member LLC taxes like this:

Money may stay in the LLC—but income still flows on paper to each owner for tax purposes.

Income Allocation and the Role of Schedule K-1

After the LLC’s informational return is prepared, each member receives a Schedule K-1. This is the document that tells each owner:

- Their share of income or loss

- Their share of deductions

- What must be reported on their personal tax return

You may owe tax based on your Schedule K-1, even if you didn’t take cash out of the business.

This is why coordination among members matters—and why cash planning cannot be done casually in a multi-member LLC.

⚠️ Pro Tip: Never Assume a 50/50 Split

Never assume profits, losses, or distributions are automatically split 50/50.

Your Operating Agreement must explicitly define:

- How profits and losses are allocated

- How and when distributions are made

- Whether ownership percentages match cash distributions

When allocation rules are unclear or ignored, tax reporting becomes confusing, and disputes between members become more likely.

The Self-Employment Tax Reality for Multi-Member LLCs

In most cases:

- Members who actively participate in the business pay self-employment tax on their allocated share of income

- This applies regardless of how much cash they withdrew

- Passive members may be treated differently depending on involvement

Self-employment tax is tied to earned income shown on the Schedule K-1, not just distributions.

This is why members can face tax bills that feel disconnected from their bank activity—and why disciplined cash planning matters.

How Owners Are Paid in a Multi-Member LLC

Owners are typically paid through distributions, not salaries.

Key discipline rules:

- Distributions should follow ownership or Operating Agreement terms

- Transfers should be labeled clearly

- Reimbursements should never be mixed with owner pay

When distributions, reimbursements, and random transfers are blended together, CPA work becomes investigative instead of mechanical.

For deeper guidance, see:

Multi-Member LLC vs Single-Member LLC Taxes

Single-Member LLC (Default)

- Disregarded entity

- Income flows directly to the owner

- Fewer coordination issues

Multi-Member LLC (Default)

- Partnership taxation

- Files an informational return

- Issues Schedule K-1s

- Requires coordination, discipline, and planning

Multi-member LLCs don’t just add paperwork—they add shared financial responsibility, which magnifies the impact of poor money management.

EIN Requirement for Multi-Member LLCs

A multi-member LLC must have an EIN.

The EIN is required to:

- File partnership returns

- Issue Schedule K-1s

- Open business bank accounts

- Establish financial separation

Without an EIN, proper tax and banking compliance is impossible.

For full details, see:

→ Do You Need an EIN for an LLC?

Common Multi-Member LLC Tax Mistakes

Most issues come from misunderstanding how allocation works.

Common mistakes include:

- Assuming tax is owed only on distributions

- Ignoring Schedule K-1 income

- Taking uneven distributions without clarity

- Mixing reimbursements and owner pay

- Weak banking and recordkeeping discipline

Each mistake adds ambiguity. Over time, ambiguity increases CPA fees, delays filings, and raises compliance risk.

Why Banking and Money Management Matter for Taxes

Taxes reflect behavior throughout the year.

- Poor banking structure creates unclear records

- Weak money flow discipline complicates allocations

- Inconsistent owner pay makes K-1 reporting harder

That’s why taxes cannot be separated from banking structure and money management behavior.

To strengthen the foundation:

Reducing Tax Friction Without Complexity

Multi-member LLCs don’t reduce tax risk by being clever. They reduce it by being clear.

Clarity comes from:

- Defined allocation rules

- Disciplined cash planning

- Intentional owner pay

- Clean banking structure

- Consistent records

When these are in place, Schedule K-1s stop being surprises and tax season becomes predictable.

Where to Go Next

To continue building a solid financial and compliance foundation, explore the LLC Made Easy Education Center, which brings together step-by-step guides on LLC banking, money management, owner pay, and tax structure.

Together, these guides form a complete system for managing multi-member LLC taxes intentionally instead of reactively.

Disclaimer

This content is provided for general educational purposes only and does not constitute legal, tax, accounting, or financial advice. Tax laws and individual circumstances vary. Consult a qualified CPA or attorney for guidance specific to your situation.